Real estate leasing companies in a fix over blocked credit eligibility

Commercial real estate developers leasing their properties are receiving notices about blocked credit eligibility under sections 17 (5) C and 17 (5) D even as the case is being argued at the Supreme Court, say real estate industry stakeholders.

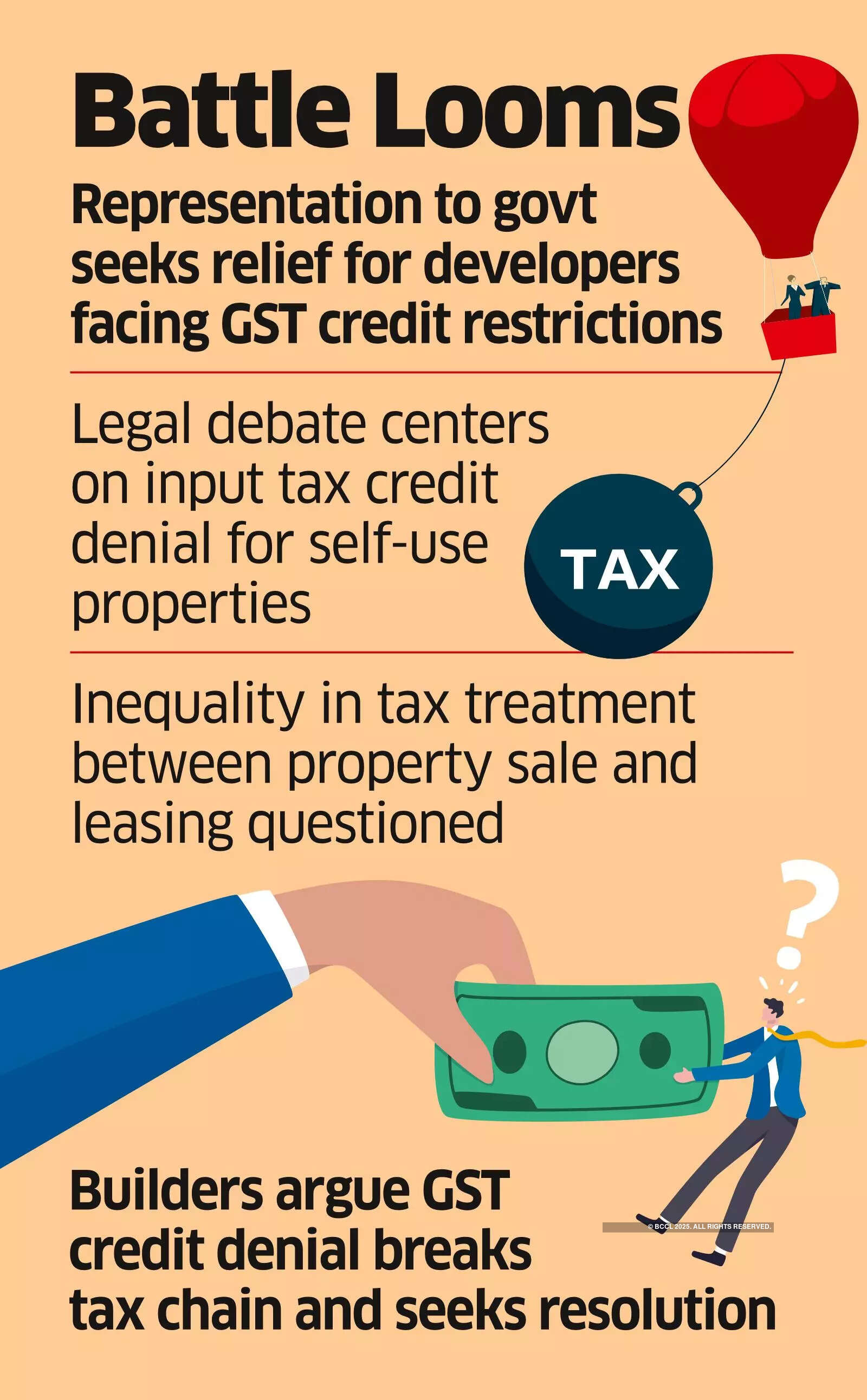

If a developer constructs a commercial building and sells it before obtaining an occupancy certificate, they may be eligible to claim credit, provided they pay the output GST on the sale transaction.

However, if the developer uses the building for leasing, such an ITC is not available for set-off.

“This impacts the overall business as this increases the cost of construction, thereby increasing rentals. Multiple representations have been sent to the government, but developers have yto get any relief. As India is becoming the preferred choice for office space and global capability centres for MNCs who typically prefer to lease property, such an anomaly tends to impact the economics of operating in India negatively,” said Gaurav Karnik, national leader, real estate, EY India.

According to one such representation by CII, construction costs typically account for 32% to 38% of the total project cost, and given that GST is applicable at the rate of 18% on such services (which becomes the cost for the company), there is a significant cost that the industry bears due to the specific restriction on the availment of ITC.

“The moot point before the court is whether input tax credit can be denied when goods and services are used for the construction of the building on own account. These buildings are used by the businesses for rendering output services such as leasing, hotel services, and warehouse services”, explained Abhishek A. Rastogi, founder of Rastogi Chambers, who is arguing the matters before the Supreme Court and various high courts.

Both sale and leasing are different ways to monetize value from the property; however, the tax treatment is different, as is the tax burden, which is against the principles of equality, experts said.

“A builder who sold the office or retail asset is unable to attract global brands as they prefer property on lease directly from builders. This is why most of the big developers have started leasing mall and office space. However, one major hinderance to this development is the denial of ITC, which impacts the overall cost of the project, and the government should look into it,” said Harsh V. Bansal, convenor of the CII Delhi Sub-committee on Real Estate, Urban Development, and Infrastructure and co-founder of Unity Group.

The builders say that credit is their vested right and any denial will break the tax chain, which is against the GST.

“The taxpayers can avail the credit in the time frame prescribed under the statute, and if show cause notices have been issued for recovery of the input tax credit availed but not utilised, then it may be imperative for such taxpayers to obtain a stay on recovery through such notices”, Rastogi said.

CII had said that the government needs to relook at the GST regime for the leasing segment, which restricts the claim of ITC on goods and services used for the construction of immovable property even though the same are used for providing taxable services in commercial leasing.